The YEI Finance token has a price chart that looks like a recovery story. From its low near $0.05 in February 2026, CLO climbed back to $0.27, a 307.6% gain in thirty days that put it among the top-performing assets on BNB Chain this month. The market cap sits at $35.3 million. The community sentiment on CoinGecko is 100% bearish. Those two data points rarely share a page.

The protocol recently rebranded under the name Clovis, positioning itself as a cross-chain clearing layer. That narrative is what the price action appears to be riding. The on-chain data tells a different story about where the token has been and who currently controls it.

CoinGecko: CLO price $0.27, +307.6% in 30 days, $35.3M market cap, community 100% bearish. Source: coingecko.com/en/coins/yei-finance

What the Protocol Actually Looks Like Right Now

YEI Finance launched in November 2025 as a BNB Chain lending protocol. CLO went from zero to an all-time high near $0.80 in January 2026 before collapsing 94% to near-zero by February. The current recovery to $0.27 is what the 307% thirty-day figure reflects – it is a rebound from near-zero, not growth from a stable base. The full price history is visible on the CoinGecko max chart.

CoinGecko max chart: Launch Nov 2025, ATH ~$0.80 Jan 2026, collapse to near-zero Feb 2026, current partial recovery to $0.27. Source: coingecko.com/en/coins/yei-finance

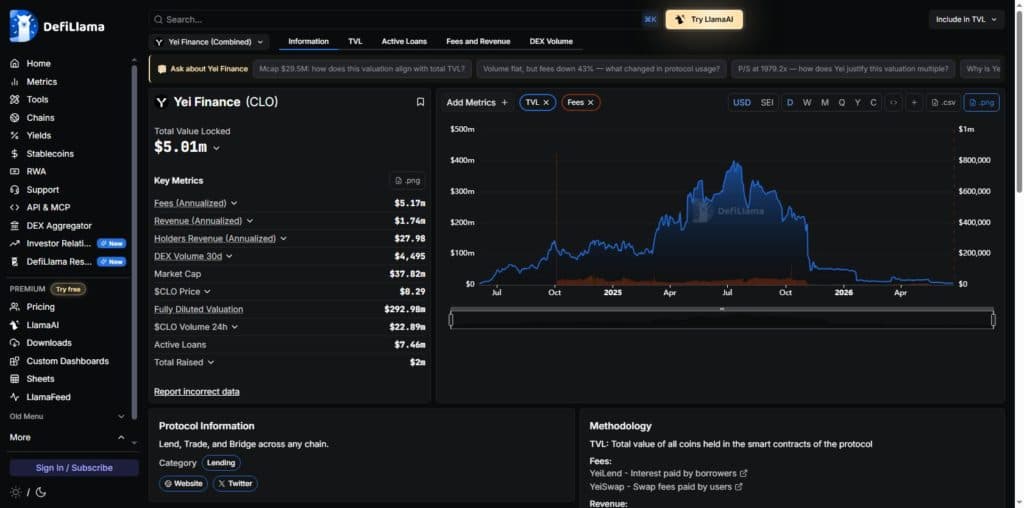

At its peak in mid-2025, the protocol held approximately $400 million in total value locked across its lending pools according to DeFiLlama. By June 2026, that figure stands at $5 million. The decline from peak to current is 98.75%. Protocol revenue followed the same trajectory – quarterly fees that exceeded $3.35 million in 2025 have fallen to roughly $76,000 in Q1 2026. Against a $35.3 million market cap, the current annualized revenue produces a price-to-sales ratio above 1,900x.

DeFiLlama: YEI Finance TVL collapsed from ~$400M peak (mid-2025) to ~$5M current (-98.75%). Fee income follows the same trajectory. Source: defillama.com/protocol/yei-finance

For context, a P/S ratio above 1,900x means the market is pricing the token as if it expects revenue to grow roughly 1,900 times from its current level. There is no evidence in the protocol data that this growth is underway. DEX volume for CLO runs at levels consistent with approximately $4,495 per month.

CoinGecko stats panel: FDV $274.5M, FDV/MC ratio 7.8x, TVL $3.9M. Only ~13% of total supply currently circulating. Source: coingecko.com/en/coins/yei-finance

A Rebranding Without a Rebuild

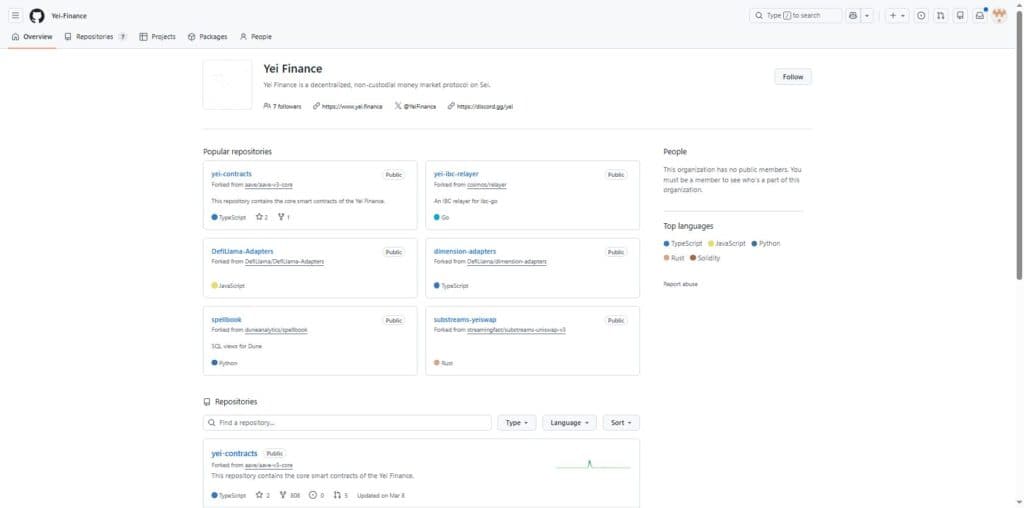

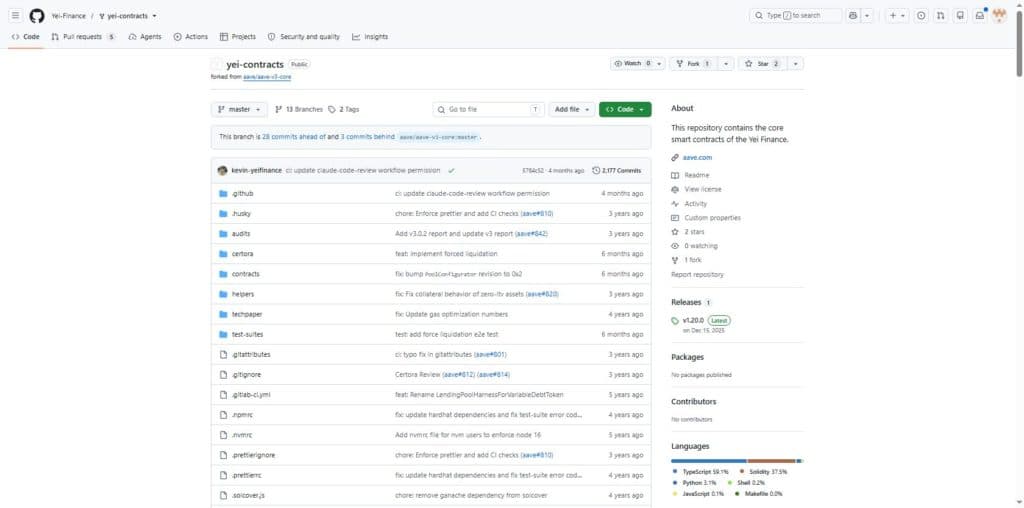

The technical case for the Clovis cross-chain clearing narrative requires examining what changed in the codebase when the rebrand happened. The GitHub organization for YEI Finance shows multiple repositories, none of which contain original code. Every repository is a fork – primarily Aave v3 and Morpho lending infrastructure with interface modifications. The most recent commit to the primary contracts repository dates to approximately February 2026, four months before this writing.

GitHub org overview (github.com/yei-finance): All repositories are forks. No original protocol code. Anonymous team with zero listed contributors.

yei-contracts repository: Last commit ~February 2026 (4 months ago). No listed contributors. Source: github.com/yei-finance/yei-contracts

The development picture is consistent with what happens when a protocol stops being actively maintained: commits stop, contributor activity goes quiet, and the codebase freezes at whatever state it was in at the last active period. The Clovis rebrand and the cross-chain clearing positioning appeared as a narrative update, not a codebase update. There is no publicly visible technical work that would support the cross-chain infrastructure claim.

This does not mean the team has disbanded or that the protocol is contractually inoperable. It means that whatever is driving the current price move, it is not new development activity. A protocol whose GitHub shows no commits in four months and whose total value locked has declined 98.75% from peak is being priced at a market cap of $35.3 million on the basis of something other than present fundamentals.

The Wallet Nobody Can Identify

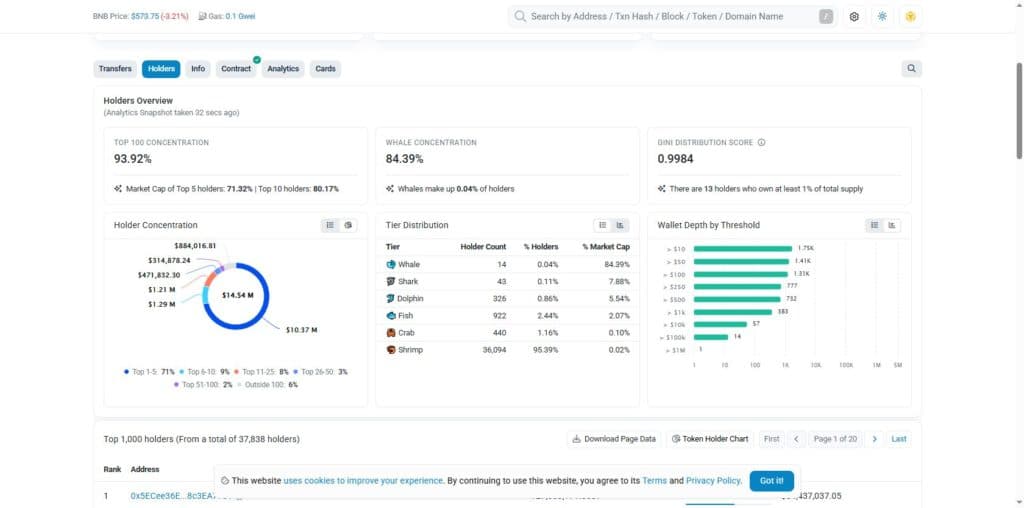

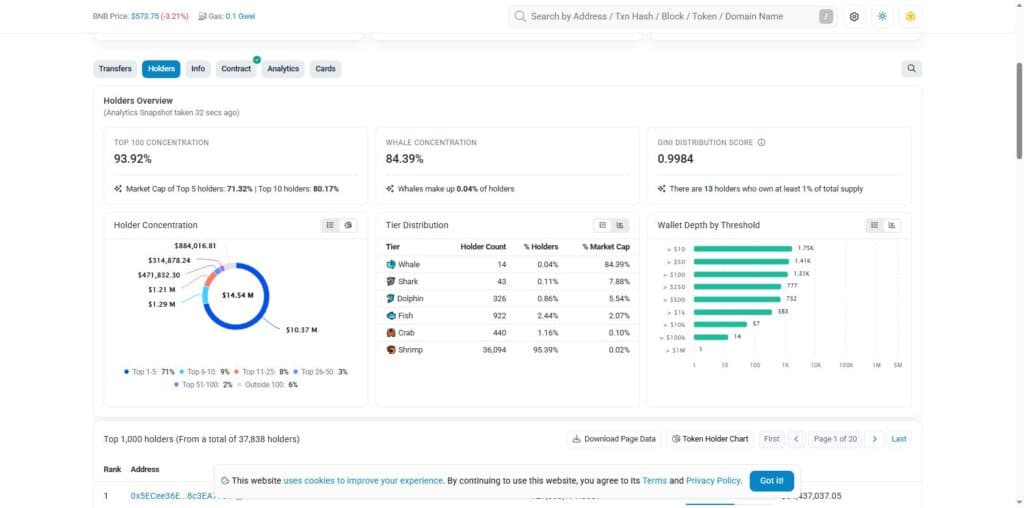

The on-chain holder data is where the CLO story becomes structurally unusual even by small-cap DeFi standards. BSCScan tracks 37,839 total holders for the CLO token on BNB Chain. Of those holders, 14 wallets classified as whales control 84.39% of the total supply. The Gini coefficient for token distribution is 0.9984. A Gini of 1.0 would represent a single entity holding everything. The current score is as close to maximum inequality as the metric can measure.

BSCScan Holders Overview: Gini 0.9984, whale concentration 84.39% (14 wallets), top 5 holders 71.32%, top 10 holders 80.17%. Source: bscscan.com/token/0x81d3a238…#balances

The most significant number in the distribution is the first one. A single wallet – 0x5ECee36E…8c3EA7781 – holds 127,003,171 CLO, representing 56.82% of all CLO in existence on BNB Chain. That position is currently worth approximately $34.4 million at current prices. The wallet carries no label on BSCScan, meaning it has not been identified as belonging to a known exchange, protocol, team, or deployer address. It is simply the largest holder of a token with a $35.3 million market cap, and nobody has publicly identified whose wallet it is.

BSCScan top holders: #1 unlabeled wallet holds 56.82% ($34.4M). Exchange wallets at #3 (Binance Alpha), #4 (KuCoin 47), #5 (MEXC 5), #7 (KuCoin 48), #8 (MEXC 13). Source: bscscan.com/token/0x81d3a238…#balances

The rest of the top holder list is a mix of identified exchange wallets and unlabeled addresses. Positions three through eight and twelve and fourteen are labeled as KuCoin wallets, MEXC wallets, and the Binance Alpha 2.0 Router Proxy – consistent with a token listed on major centralized exchanges. What distinguishes CLO is the combination of that significant CEX presence alongside an unlabeled address controlling more than half the supply. The full holder distribution is visible on the BSCScan token holders page.

The Supply Figure That Does Not Match

CoinGecko reports CLO circulating supply as 129,100,000 tokens and total supply as 1,012,672,000 tokens. The implied fully diluted valuation at current prices is $274.5 million, producing an FDV-to-market-cap ratio of approximately 7.8x. That ratio indicates only about 13% of the total token supply is currently counted as in circulation.

BSCScan shows the token contract has minted 223,516,229 CLO on BNB Chain. That figure is 73% higher than the 129.1 million reported as circulating supply by CoinGecko. The gap between on-chain total supply and reported circulating supply is approximately 94.4 million tokens. This gap typically represents tokens held in vesting contracts, team wallets, ecosystem reserves, or protocol-controlled addresses that have been excluded from the circulating count.

The math connects to the unlabeled #1 holder. If that wallet at 127 million CLO represents a treasury or vesting address, it would account for most of the gap between on-chain supply (223.5M) and reported circulating supply (129.1M). But no public documentation from the project confirms this interpretation. The wallet has no label, no associated announcement, and no disclosed unlock schedule. Whether it begins selling into the current pump – which would represent a sell pressure of $34.4 million against a $35.3 million total market cap – is unknown.

The Price Action Without an Explanation

CoinGecko 3-month chart: CLO recovery from ~$0.05 ATL (Feb 2026) to current $0.27. The 307.6% gain is measured from the February low. Source: coingecko.com/en/coins/yei-finance

The three-month chart shows CLO moving from the February 2026 floor of approximately $0.05 upward in a recovery that accelerated in late May and June 2026. Community sentiment on CoinGecko remains 100% bearish even as the token tripled. Existing holders who bought near the ATH at $0.80 and held through the 94% collapse have little reason to feel optimistic about a recovery to $0.27. The current buyers may be a different cohort – traders responding to the Clovis rebrand narrative without examining whether the protocol infrastructure supports that positioning.

The most straightforward reading of the available data is a protocol that peaked in mid-2025, saw TVL and revenue collapse through the second half of the year, rebranded with a new narrative in early 2026, and is now experiencing a price recovery on the back of that narrative while the underlying fundamentals – TVL at $5 million, fees at $76,000 per quarter, no new code commits in four months, one unlabeled wallet holding 56.82% of supply – have not materially recovered.

What changes that picture is either evidence of real cross-chain infrastructure being built (new commits, new contracts, new technical announcements), TVL returning to the protocol, or the identity and intent of the #1 holder becoming known. Until one of those things happens, the gap between the price chart and the protocol data is the story.