Seven months ago, Strategy told investors its Bitcoin reserves could cover preferred stock dividends for 71 years. That number now sits at 31.6 years.

More than half the runway vanished. And the shrinking hasn’t stopped.

On X, Coin Bureau flagged the collapse in coverage, noting how the 71-year figure from last November has dropped to roughly 32 years today. The post pointed to CryptoQuant analyst Julio Moreno, who warned that the decline could accelerate if Strategy starts selling Bitcoin to fund its payouts.

The Math That Keeps Getting Worse

Strategy’s own dashboard confirms the data. The company holds 846,842 BTC valued at $54 billion. Annual dividend obligations sit at $1.711 billion. BTC years of dividend coverage: 31.6. USD months of coverage: just 7.7.

That USD figure is the one that should concern STRC holders more than anything.

STRC, Strategy’s perpetual preferred stock, currently pays an 11.50% annual dividend. It trades at $89, well below its $100 par value. Effective yield has climbed to 12.92% because of that discount. The next payout date is June 30, 2026.

For a retail investor holding STRC for that monthly yield check, the question isn’t whether Strategy has enough Bitcoin on the books. The question is whether it can keep converting reserves into cash without triggering the very problem it’s trying to avoid.

A Spiral Nobody Wants to Name

Julio Moreno’s warning, as highlighted by Coin Bureau on X, cuts to the core of the risk. If Strategy sells Bitcoin to pay dividends, that selling creates downward pressure on BTC price. A lower BTC price reduces the dollar value of Strategy’s reserves. Reduced reserves mean the years of coverage shrink faster.

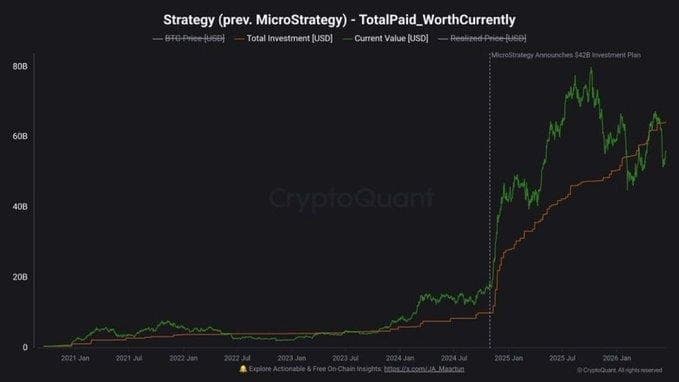

CryptoQuant data showing Strategy’s total investment versus current Bitcoin value over time. Source: CryptoQuant

It loops back on itself. Sell to pay, price drops, coverage shrinks, need to sell more. Moreno has previously told The Block that Bitcoin could trade between $70,000 and $55,000 in a sustained bear market. BTC currently trades near $63,842.

Strategy already broke its no-sell rule. On June 1, 2026, the company disclosed a sale of 32 BTC for $2.5 million to cover routine preferred dividend payments. It was tiny. Just 0.0038% of its total holdings. But it happened.

71 Became 49 Became 32

The speed of the decline tells its own story. In November 2025, Strategy claimed 71 years of BTC dividend coverage. By April 2026, that had fallen to about 48.7 years according to the company’s dashboard at the time. Now in June, it reads 31.6.

Three data points in seven months. Each one lower than predicted.

MSTR shares closed at $116.56, down 5.09% on the day. Market cap sits at $41.5 billion. The stock’s one-year return is negative 69%. Enterprise value stands at $62.6 billion with $6.75 billion in debt and $15.4 billion in preferred stock obligations.

Strategy’s mNAV ratio, the multiple of its market cap to net asset value, was 1.16 as of June 17. That has fallen 2.52% from the previous close. When mNAV approaches 1.0, the premium that MSTR commands over its Bitcoin holdings vanishes. For a company whose entire model depends on issuing stock at a premium to buy more BTC, that compression is a structural threat.

Where Cash Actually Stands

The company’s USD reserve is listed at $1.1 billion. Against $1.711 billion in annual dividends, that’s 7.7 months of cash coverage before Strategy needs to either sell BTC, issue more equity, or tap the STRC ATM program.

CEO Phong Le said during the Q1 2026 earnings call that Strategy would sell Bitcoin when it is to the company’s advantage. Michael Saylor framed it as evolution. The old pledge was binary: never sell. The new stance is tactical.

STRC’s 30-day average trading volume runs at $367.2 million. Historical volatility sits at 21.3%. For a security designed to strip away Bitcoin volatility and trade near par, dipping to $89 represents a meaningful gap. Buyers at that price are getting compensated for risk that wasn’t in the original pitch.

What African Trader Sees Differently

Most coverage from CoinDesk and Decrypt focuses on U.S. institutional holders and MSTR as a leveraged Bitcoin proxy. But in Nairobi, Lagos, and Accra, retail traders bought STRC through international brokerages specifically for the monthly dollar-denominated yield. For someone earning in Kenyan shillings or Nigerian naira, an 11.5% USD yield felt like a hedge against local currency devaluation.

That calculus changes fast when the instrument trades 11% below par and dividend coverage keeps dropping. A forced BTC sale large enough to move price would hit these holders twice. Once through STRC’s value. Again through their separate Bitcoin positions.

Net leverage across Strategy’s balance sheet is listed at 10%. Amplification, the ratio of preferred stock to total Bitcoin backing, sits at 41%. Those numbers look manageable in isolation. But coverage metrics that halve in less than a year aren’t isolated.

The 71-year claim from November 2025 was built on Bitcoin sitting above $90,000 and preferred obligations being smaller. Both conditions reversed. BTC dropped below $64,000. Preferred stock issuance ballooned as Strategy tapped ATM programs to fund more purchases. The denominator grew while the numerator shrank.

Coin Bureau’s post on X, citing Moreno, didn’t say the dividends will stop. It said the trajectory has a direction. And right now, that direction doesn’t bend back on its own without a Bitcoin price recovery.