David Hoffman held Ethereum for nine years. He built a career on it, a media company around it, and an identity through it. Then, on May 21, 2026, he sold it all.

The move did not come quietly. As Hoffman, co-founder of Bankless, posted on X, the decision was not about giving up on Ethereum as a network. It was, he said, about what the ETH money thesis was always going to deliver. And in his reading, it already has.

But not everyone agrees with that reading.

What Nine Years of Diamond Hands Actually Concluded

Hoffman’s thesis was built on a specific chain of events all working in sequence. Ethereum’s leadership needed to stay credibly neutral. Its L2 ecosystem had to remain economically tied to the base layer. Apps and rollups had to scale without bleeding value away from ETH itself. And the whole thing had to happen fast enough to outrun competitors before blockspace became a commodity.

It did not play out that cleanly. Solana rose through 2021, pulling developer attention and fee revenue. L2s scaled activity but passed the margins elsewhere. The stablecoin ecosystem, now sitting at $163 billion on Ethereum’s rails, strengthened the dollar’s global position more visibly than it strengthened ETH’s price.

As David Hoffman posted on X on May 26, 2026:

“The ETH is Money thesis didn’t fail… it played out. Ethereum got the ETH price it deserves, and I don’t see ETH being rerated as an asset, higher or lower.”

He is also, notably, still bullish on Ethereum the network. The distinction matters. His argument is not that Ethereum failed. It is that Ethereum’s architecture is designed to give value away, to its L2s, to its apps, to its ecosystem. ETH captures the minimum. That is a feature, Hoffman said, not a bug. But it makes a compelling investment thesis harder to construct.

He held for nine years. That part gets lost in the coverage.

The Counter-Trade Nobody Is Running Headlines On

While Hoffman’s exit dominated feeds across crypto Twitter for 48 hours, a different call was getting less noise. Crypto trader and chart analyst Alicharts, posting on X, laid out a specific on-chain case for accumulating ETH at current levels, not shorting it, and not selling it.

The setup Alicharts described starts with a rejection at the mid-range of a multi-month channel, which coincided with the 200-week simple moving average. Price could still move lower. The $1,560 level is on the table. So is $1,070 if the lower channel boundary gives way.

But the case for buying is not a price prediction. It is a metric called the MVRV pricing bands. Historically, when Ethereum drops below the 0.8 MVRV band, the price does not stay there long. As Alicharts posted on X:

“Rather than risking capital trying to perfectly time a short into a historic value zone, my approach is to remain patient with the long-term thesis and gradually accumulate through structural weakness.”

That is a different frame than Hoffman’s. Hoffman is asking whether ETH will ever receive a structural rerating. Alicharts is asking whether the current price zone is historically cheap. Both questions can be right at the same time. Kenyan retail traders watching ETH from platforms like Binance, where entry at $2,100 feels already steep, may find the Alicharts framing more directly useful.

This is not a single-direction story.

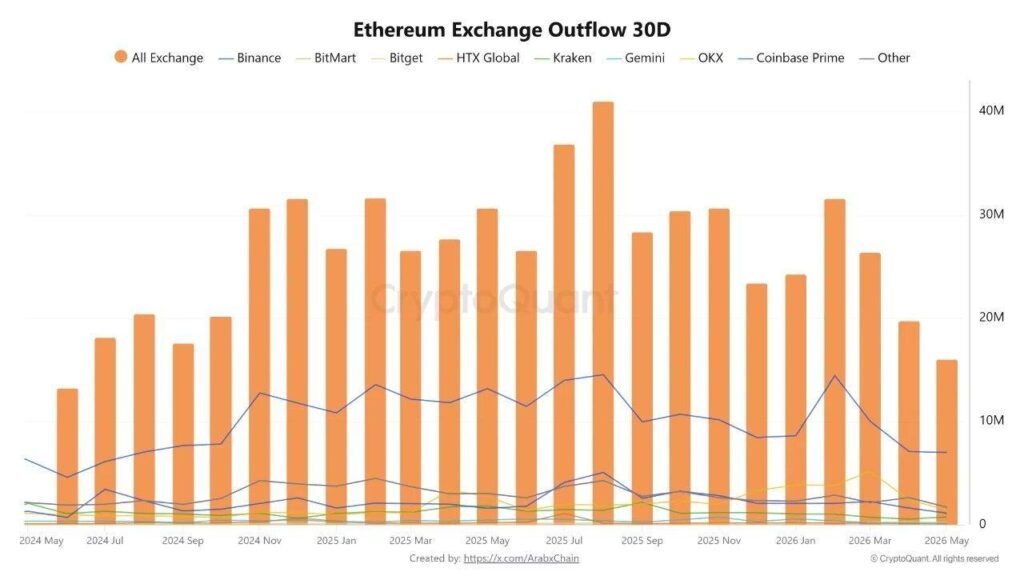

What the Exchange Flow Charts Are Actually Saying

The on-chain picture adds a third dimension to this debate. CryptoQuant data published this week shows Ethereum’s 30-day exchange outflow indicator dropped to approximately 16.05 million ETH, the lowest reading since June 2024. Binance led the period with around 7.00 million ETH in withdrawals. OKX came in second at roughly 1.43 million ETH, and Coinbase Prime third at about 1.12 million ETH.

Ethereum Exchange Outflow 30D — Source: CryptoQuant

The chart tells something specific. Peak outflow activity, which signals ETH moving off exchanges into self-custody or long-term storage, hit its highest points through mid-2025. Since then, the trend has reversed hard. The 16.05 million ETH figure represents a period where fewer coins are leaving exchanges, not more.

A drop in exchange outflows is not automatically bearish. But it does indicate a slowdown in the kind of conviction-buying that drives long-term price support. When holders stop pulling coins off exchanges, it suggests a wait-and-see stance rather than a confident accumulation posture.

The timing of that slowdown lines up almost exactly with the period Hoffman describes as the closing of the ETH rerating window. That may be correlation. It may not be.

Nine years of conviction built that outflow trend. Something stalled it.

Ryan Sean Adams Had Something to Say About the Timing

Hoffman’s co-founder at Bankless, Ryan Sean Adams, did not stay quiet. As Ryan Sean Adams posted on X on May 26:

“Either this or, it’s just taking longer than you thought.”

Hoffman responded directly, saying a core part of his argument is that ETH lost momentum, and in the coordination game of money, lost momentum may be an existential condition, not a temporary setback.

The broader reaction was split. One account, posting on X under the handle 0xMakesy, framed the tension between Ethereum’s original vision and what it became. Ethereum, he argued, was always the stronger, more ideologically pure version of crypto, built for its own sake. The weaker version, efficient ledger infrastructure for financial institution backends, was supposed to feed inflows into the stronger one. Instead, Ethereum’s stablecoin utility is now actively serving US dollar dominance strategy.

That argument, surfaced in a post from 0xMakesy on X, gets closer to the actual structural debate than most of the takes circulating this week. It is not about whether ETH is cheap. It is about which version of crypto the last five years validated.

The stablecoin figure is hard to dismiss. $163 billion, up from $3 billion in 2020. That is a 54x expansion, built on Ethereum’s rails.

The Number That Changes the Calculation

Bitcoin open interest climbed 12% to $18.4 billion on May 13, 2026, per Coinglass data, reflecting conditions across the broader market that context ETH’s current position. ETH, trading near $2,100 at the time of writing, has not broken past the $2,200 zone with any conviction through May.

The on-chain MVRV data Alicharts referenced points to conditions that have historically preceded recoveries. That does not mean the current dip resolves upward. The $1,560 level Alicharts flagged as a potential downside target would represent another 25% drop from current prices, a scenario that would test even the most patient accumulation thesis.

What ties the two sides together is the exchange outflow chart. When conviction was high, coins left exchanges at 35 to 40 million ETH in 30-day windows. That figure is now 16.05 million ETH. The drop reflects a market still deciding what ETH is in 2026, even as some of its longest-standing advocates have made their call.

Hoffman holds nine years of firsthand experience on that question. The data he referenced about L1 fee correlation, Solana’s 2024 revenue-driven rerating, NEAR’s 2026 price action alongside burn growth, these are not abstract arguments. They are market outcomes.

Both the seller and the buyer are looking at the same asset. They are drawing different conclusions from it.